Written by Field Name

Report Date

5 min read

On 26 May 2021, a Dutch court ordered Shell to reduce its global carbon emissions by 45% by 2030 from 2019 levels. Notably, the scope included the emissions of Shell’s suppliers and buyers. Shell’s CEO Ben van Beurden responded in the weeks following,

“Now we will seek ways to reduce emissions even further in a way that remains purposeful and profitable. That is likely to mean taking some bold but measured steps over the coming years.”

Shell is not alone in being required to take bold but measured steps. With the massive surge in ESG investment, investors are seeking assurance that company value chains are not linked to carbon intensive technologies.

The questions stands:

How are those steps to be determined and measured in a world where Scope 3 emissions accountability, such as that which is being required of Shell, is increasingly being demanded?

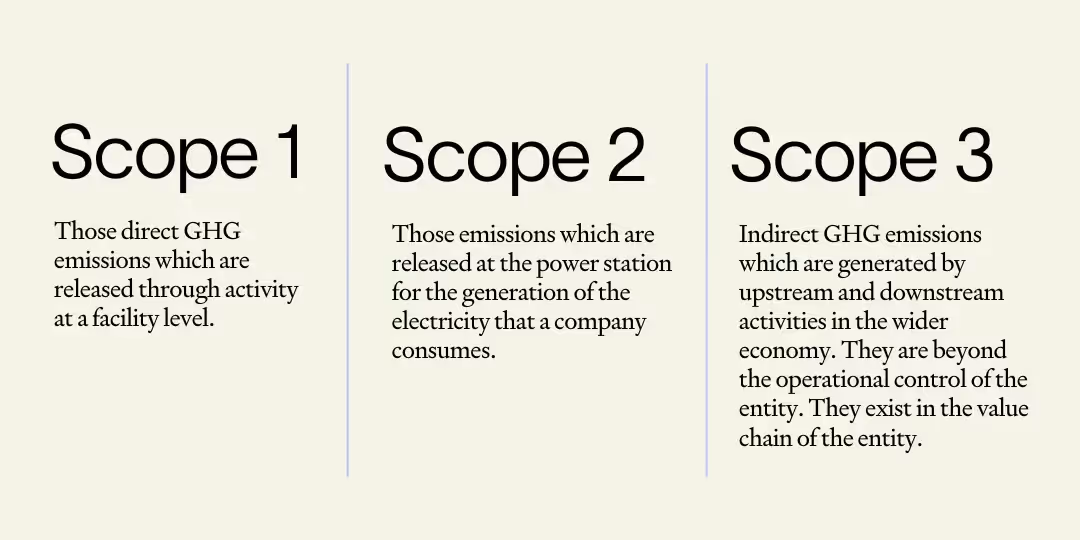

Measuring Scope 3 emissions is difficult. This situation is exacerbated by lagging carbon accounting systems, such as those in Australia, designed around last century concerns and limited to Scope 1 and Scope 2 considerations. What new tools and methods are needed?

According to Australia’s National Greenhouse and Energy Reporting (NGER) organisations should quantify Scope 1 and Scope 2 emissions.

Scheme Scope 3 emissions are not reported under the NGER Scheme.

Because Scope 3 data lies in the supply chain rather than in the operations of an entity, measuring it becomes more difficult. Scope 3 data are very hard to assess, because both upstream and downstream emissions occur in millions – if not billions – of supply chains. As a result, reported Scope 3 emissions often rely on certain assumptions and subjective biases – but unlike Scopes 1 and 2, they are so far not required to follow rigorous, unified reporting standards.

This lack of transparency regarding the reporting approaches renders most Scope 3 data with a high degree of uncertainty. This uncertainty is compounded by differing methodologies across ESG rating providers making E scores problematic and any material comparison, either financially or environmentally, fraught.

Is there an alternative?

ESG risks, such as Scope 3 emissions or indeed forced labour, as discussed in our ‘Exposures to Forced Labour in the Supply Chain of Clean Energy’ Report, are often hidden deep in supply chains.

Fair Supply’s solution is to apply input-output technology to the problem.

We use global trade flow data to analyse the supply chain (up to tier 10) of the following security types: listed equities, private equities, infrastructure assets and sovereign bonds. We provide visibility up to tier 10 of the supply chain, to identify GHG emissions within the supply chain of an entity’s products, services and investors.

1. We compare apples with apples, meaning that every client gets assessed according to the same methods, scope, and using the same supply chain data. For the first time, Scope 3 data become comparable.

2. The supply chain assessment is not based on biases, but purely based on publicly available national accounting and trade data.

3. Mathematically, our approach does not have boundaries, meaning that we are actually assessing all upstream and downstream

4. The methodology is well-established, especially for environmental problems and within academia. (Wassily Leontief, who first proposed input-output analysis, received the Nobel Prize for it in 1973.)

Scope 3 emissions lie outside the operational control of an entity, yet they are increasingly being scrutinised. Supply chain visibility is proving crucial. Importantly, Scope 3 emissions may represent the bulk of an entity’s GHG emissions. As such, they offer a significant opportunity for emission reduction, if the right means of engagement with buyers and suppliers are employed.

This Report is prepared by Fair Supply Analytics Pty Limited.

ACN 637 115 587 (FairSupply)

1.1 FairSupply is not a financial or legal adviser and we have not considered any accounting, commercial, technical, operational, tax or financial matters. The information contained in the Report is not financial product or legal advice and does not consider your investment objectives, financial situation and particular needs (including financial, accounting, legal and tax issues).

1.2 Before acting on any information provided by FairSupply in this Report or in the Report Content, you should obtain independent professional advice and consider the appropriateness of the advice for you, having regard to your own circumstances.

1.3 FairSupply has used its best endeavours to ensure all information in this Report are correct and up-to-date at the time of publication. FairSupply, its officers, employees and agents do not make any representations or warranties (express or implied) as to the fairness, currency, accuracy, adequacy, completeness or reliability of the Report Content or that the Report is free from any errors, omissions or defects. FairSupply, its officers, employees and agents are not liable to you for any indirect, incidental, special or consequential loss or damage, loss of profits or anticipated profits, economic loss, loss of business opportunity, loss of data, loss of reputation or loss of revenue (irrespective of whether the loss or damage is caused by or relates to breach of contract, tort (including negligence), statute or otherwise, arising out of or in connection with the Report, the Report Content or all links in the Report, including (but not limited to) for any person placing any reliance on, or acting on the basis of the Report Content.

Learn more about our ESG risk and compliance platform or get in touch with an ESG specialist today